Private Equity & Friends Fight Back Against Child Care Guardrails

Spurious arguments abound!

When Massachusetts became the first state to establish significant guardrails around large for-profit child care companies, my understanding is that institutional investor-backed chains1 and their lobbyists were caught largely flat-footed. It won’t shock you to hear they’ve since gotten their act together. I’ve been following along as the Colorado legislature has been considering a bill, HB25-1011, that would put up guardrails around these chains far more modest than Massachusetts’. It isn’t going well. (Update: On 4/9, the Colorado Senate voted down the legislation.)

One useful part of this process, though, has been observing both the House and Senate hearings, at which I testified in favor of the bill. For one of the first times, the chains and their backers showed up and made a full-throated defense not only of why investor backed for-profit chains should not be regulated differently than any other type of program, but why the presence of private equity in child care is a good thing. Some of these arguments sound compelling on their face and I can tell they are landing to some extent with lawmakers. I thought, therefore, it would be helpful to run through the chains’ playbook and explain why their assertions fall flat.

1. It’s not fair to target businesses based on ownership

This was repeated multiple times at the hearings: just because a business has a certain ownership structure shouldn’t open it up to different regulatory requirements. A typical example is when a KinderCare executive offered that the legislation “sets a dangerous precedent by singling out only 10% of Colorado's childcare ecosystem based solely on ownership structure." Of course, the government distinguishes different types of businesses in regulation all the time. It does so on size (hundreds of laws only kick in when a business has a certain number of employees), on how a given service is delivered (already in child care, family child care homes and child care centers have distinct regulations), on whether a business is a nonprofit, privately held for-profit, franchisor, or publicly-traded company subject to oversight by the Securities and Exchange Commission. This argument thus has a truthiness feel but no actual truth.

Indeed, many states are beginning to make moves to regulate investor activity—particularly private equity—differently in socially-focused sectors. We see this most clearly in health care. Massachusetts was again the pioneer here, passing “a law that will expand the state’s oversight of certain healthcare transactions by private equity and real estate investment trusts investors and change the scope of the state’s healthcare transaction review law notice and requirements to capture additional transaction types and entities.” The Oregon legislature is actively “considering a bill that would restrict private equity and corporations from controlling Oregon healthcare companies.”

I want to keep hammering this point because it is important. Again, just in 2025, New York Governor Kathy Hochul has proposed measures to curb the influence of private equity and hedge funds in the housing market. Pennsylvania Governor Josh Shapiro has asked the state legislature to pass a bill barring sale-leaseback arrangements and other financial machinations by private equity in health care; Shapiro wrote in a budget document, “It’s time for us to stand up for local hospitals and nursing facilities, and put in place real safeguards against private equity.” Heck, even the National Football League put guardrails around private equity firms (guardrails which do not exist for other types of would-be owners) when they allowed those entities to begin purchasing stakes in teams.

Why, then, should child care be the only social sector where institutional investors like private equity are allowed to operate unfettered? No, it is proper to consider ownership structure as part of a regulatory regime. It’s actively called for, I’d argue, when certain ownership structures introduce a strong profit-maximization motive for companies that operate in a socially important sector like child care (and also one where providers frequently access public funds).2 Many if not most regulations certainly make sense to apply across the board, but extra scrutiny and oversight for investor-backed companies is appropriate—indeed, it is necessary.

2. Investor-backed programs are only a small portion of the sector

The next argument in the playbook basically boils down to ‘why are you picking on little ol’ us?’ Since investor-backed chains only make up around 10% of the child care sector, the logic goes, it’s a waste of time to focus on them. Worry about the other 90%!

An aside: remember all the concern above around private equity in health care and nursing homes—all the legislative action and lobbying and big-state governor involvement? Quick, without looking, guess: what percentage of private hospitals are owned by private equity firms? What percentage of nursing homes?

…

It’s 8% of private hospitals and 5% of nursing homes. Hmm.

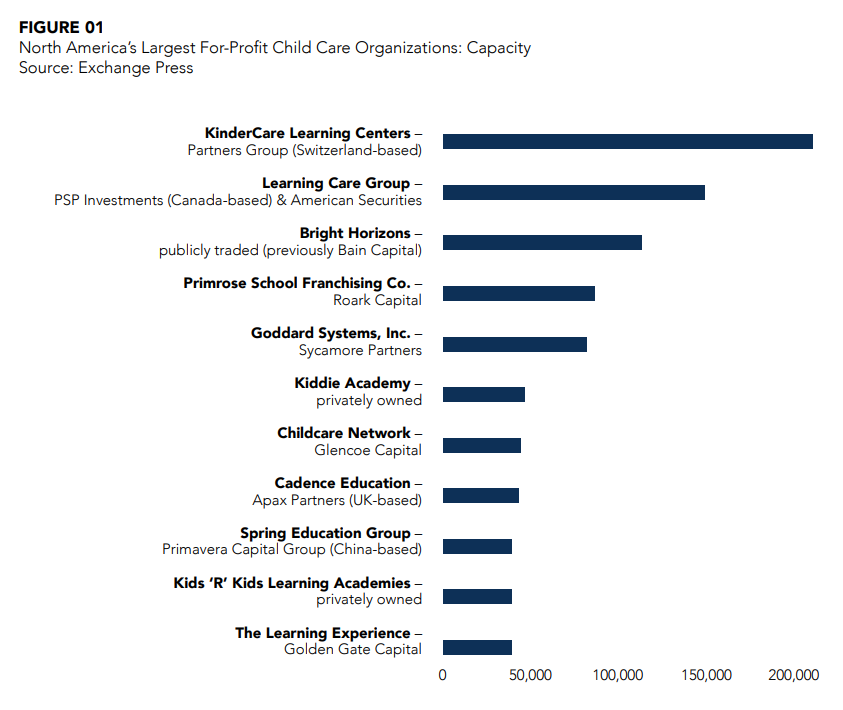

The market-share argument is hollow for a couple reasons. First of all, that 10% is concentrated in the hands of a small number of companies who have a tremendous number of sites—KinderCare alone serves over 200,000 children and has more capacity than most small states!—which means there is a compelling public interest in the financial health and operations of these companies (which, again, can and do collapse). It’s not dissimilar to saying that it doesn’t really matter what Idaho is doing because Idaho only contains 0.6% of the U.S. population.

The other piece of the puzzle is that this is 10% of the sector with massively outsized political power. I’ve written before that, “Many private equity firms also have a history of getting involved in politics to protect their investments, actions which are not always aligned with the public interest: as [Plunder author Brendan] Ballou writes, ‘quite simply, Congress works for few constituencies harder than it works for private equity.’” This includes spending $54 million in 2019 successfully lobbying against legislation that would have curbed surprise medical billing because private equity owned most of the medical billing companies. Why, again, do we think that child care is the only sector where private equity and other institutional investors would not protect their own business interests, whether or not those interests are aligned with what’s best for children, families, and child care educators?

In short, not all market share percentages are created equal.3 The degree of market penetration is not a legitimate defense against oversight.

3. Investor-backed programs can be high quality

Another common line is that investor-backed programs can be high quality offerings, with many of them bearing accreditation from national organizations. And if the product is high quality, why the concern? The problem is, this argument is an immaterial feint.

I don’t want to get into a debate about quality, both because quality in child care is hard to define/measure and because the picture is exceptionally messy. As I’ve written, beyond any comparisons with independent or nonprofit programs, there’s a huge amount of intra-chain variation in quality: “For instance, of the KinderCare sites listed in Illinois’ ‘ExceleRate,’ rating database, 26 are rated ‘gold circle of quality,’ 9 are rated ‘silver circle of quality,’ and 63 are in the ‘licensed circle of quality,’ meaning they meet Illinois’ licensing requirements but most staff have not taken state-approved trainings on additional quality improvement measures.” Similarly, a chunk of investor-backed sites have clean sheets when it comes to licensing violations while a chunk of them rack up repeated violations and at times end up facing the loss of their licenses.

But really, truly, it doesn’t matter.

What’s critical to understand is that there is a distinction between the pedagogical side of the chain house and the business operations side of the house. The quality of sites doesn’t matter when you have KinderCare deciding to “strategically” close nearly 400 centers(!) in the mid-2010s because the sites weren’t making enough money. The quality of sites doesn’t matter when you have Learning Care Group entering into a settlement with the Justice Department because they had a company-wide policy against administering insulin to diabetic children. The quality of sites doesn't matter when you have Guidepost Montessori abruptly closing one-third of its sites because their “hyper-scaling” strategy blew up in their faces and they couldn’t pay rent.

The guardrails that are being proposed do not hinge on whether or not a given program is high or low quality. They hinge on the fact that the profit-maximizing motives of investor-backed chains vastly increase the risk they will make business operations decisions that are harmful to the public interest or that siphon public money for undue private gain. To hold up quality as a reason to leave these chains alone is waving a shiny object in the hopes of distracting from the actual issue at hand.

4. Private equity is vital for supply

This is my least favorite, and I believe sadly most effective, argument put forth by defenders of institutional investors in child care. Speakers noted that private equity and other investment vehicles are often the only source of start-up capital in the sector, and the chains are often the only ones capable of buying up a mom-and-pop program that would otherwise close.

The problem here is that to an extent, the chain backers are correct. There are currently few other options for independent child care centers or small chains whose owners wish to sell for whatever reason. It is frequently difficult to find the start-up capital for launching a new program.

A more negative formulation of this case comes from an extraordinarily revealing piece of testimony by Dean Pappous, CEO of the private equity-owned Gardner School chain. Pappous stated before the House committee:

There's a precedent that could be set here where organizations like mine, which make decisions about opportunity costs all the time -- should we invest in Colorado or should it be in Michigan or one of our other states? -- if the standards set by this bill cause either the expense or risk to increase above and beyond where it is elsewhere for us, then I fear that our growth [in Colorado] will slow, if not stop, and then the real issue which is providing access ... will go in the wrong direction.

In other words: try to do more oversight on us, and we’ll take our ball and go home; sure would be a shame if your state’s child care shortage got worse. Gross at it may be, you can see why this angle might land with lawmakers.

However.

First of all, no one is talking about drumming institutional investors out of child care altogether, forcing them to divest their programs.4 The proposals, such as the original one in Colorado, are rather low intensity: the government wants to have a picture of your general financial health, make sure you aren’t hoarding public money for private gain, and guarantee families and staff reasonable notice if you’re planning on making an overhaul. Other regulations, like some of the ones in Massachusetts, are intended to make sure that chains which take public money aren’t being exclusionary and only serving high-income families.

If those types of common-sense, non-onerous guardrails are enough to cause a company to up and leave a state, I’d argue that reveals more about the company than the regulations. For what it’s worth, Massachusetts has not seen an exodus of programs (in fact, the state is gaining child care supply), and nearly all large for-profit operators in Canada opted into the nation’s $10 a Day system despite that system carrying plenty of restrictions on profit-maximizing behavior.

Moreover, the lack of alternative ownership transition options is a public policy problem that is solvable, not a reason why investor-backed chains should get to evade oversight. I’ll have more to say on this in the coming months, but it’s not hard to envision some version of a standing fund that allows government to purchase child care programs and turn them over to a trusted nonprofit or community-based operator, or offering grants or low-to-zero-cost loans to those types of programs which are looking to expand.

Conclusion

The challenge that private equity and other investor-backed child care chains have is that, on the merits, they hardly have a leg to stand on. They cannot explain away why child care should be the only human services sector where private equity involvement doesn’t lead to disastrously bad outcomes for the end users. They cannot explain away why financing entities whose entire reason for existing is making high returns on investment5 would be willing to trade off profit for a publicly-funded system with low parent fees and high educator salaries. They cannot explain away the concrete examples we already have of investor-backed chains acting badly as they seek more money.

Instead, we get a sleight-of-hand: don’t target us based on ownership, don’t target us because we have low market share, don’t target us because some of our programs are high quality, don’t target us because you need us. Policymakers should see through the illusion: investor-backed child care chains deserve extra oversight and guardrails. The very fact they’re protesting so loudly that they do not should give away the game.

I consider an “institutional investor-backed chain” to be any for-profit chain or franchise that is substantially backed by private equity or venture capital, or publicly traded on the stock market. Essentially, those providers that, by dint of their structure, have to be meaningfully accountable to investors/shareholders.

Some franchise owner-operators, like a Primrose or Goddard owner, make a not-unreasonable argument that they are more akin to a small business than a large chain. However, franchisees have no control over whether or not a franchisor gets into financial trouble or starts putting new profit-seeking measures in place, meaning that it is still important that franchise-model chains be included in guardrails.

Also, how long will that 10% market share stay 10%? All the chains have growth plans. And particularly if/as more public money becomes available in child care, private equity activity in other sectors strongly suggests we’ll see increased involvement. Which, by the way, begs the question: at what market share threshold do the defenders of investor-backed companies think extra oversight is reasonable? 20%? 50%? Funnily enough, they haven’t said.

Is there a future world where we have a strong publicly-funded system and I wouldn’t hate that? Yeah. But we’re nowhere close to that world.

As a recent Bain & Company report stated, “Investors want to know that a [general partner, the private equity firm member who runs the investment fund] has a reliable model for outperforming in a competitive market.”

Thank you your continued coverage on private equity’s advance in early care and education. I could not agree more with you about strategic oversight being needed, even more than what has been proposed.

My concern is for the mom and pop child care programs that need to exit due to age or the other many reasons small programs must close their doors. There are very few buyers for these people, who in many cases have poured their lives and ties their livelihoods to caring for children and families. They don’t have a support system, and they need to be able to cash out. Private equity organizations are in many cases the only potential buyers. Sadly, while I have no insights about the deals these programs close when they sell to private equity firms, but I am willing to bet Mom and Pop get the short end of the stick. Can you cover some case studies or otherwise provide Insights about how these programs fare? I am curious about what other options small programs have when it is time to move on. Thank again for incredible coverage.

Fran Simon, M.Ed.